It is often counterintuitive that a company’s owners – its shareholders – can have only a limited relationship with the body charged with overseeing management and accountability: the Board of Directors. As expectations around governance, sustainability, and long‑term value creation rise, this gap is not tenable. For industry veteran David Salmon, President of Laurel Hill Advisory Group Canada, the expectation is clear: “Thoughtful and structured Board‑Shareholder engagement has become an essential governance practice, not a niche exercise.“

Board-Shareholder engagement (BSE) is no longer a periodic exercise confined to proxy season or moments of crisis. At its core, it is an ongoing, purposeful dialogue between a company’s Board and its key long‑term investors, focused on governance, oversight, risk and value creation. As investors increasingly view Boards as accountable stewards of these issues, they expect direct access to directors to understand not just what decisions are made, but how and why they are made.

Effective BSE is proactive rather than reactive, strategic rather than transactional and should be focused on building understanding and trust over time. By engaging with shareholders and stewardship teams, Boards can explain their governance philosophy, listen to investor perspectives, and reduce reliance on external interpretations.

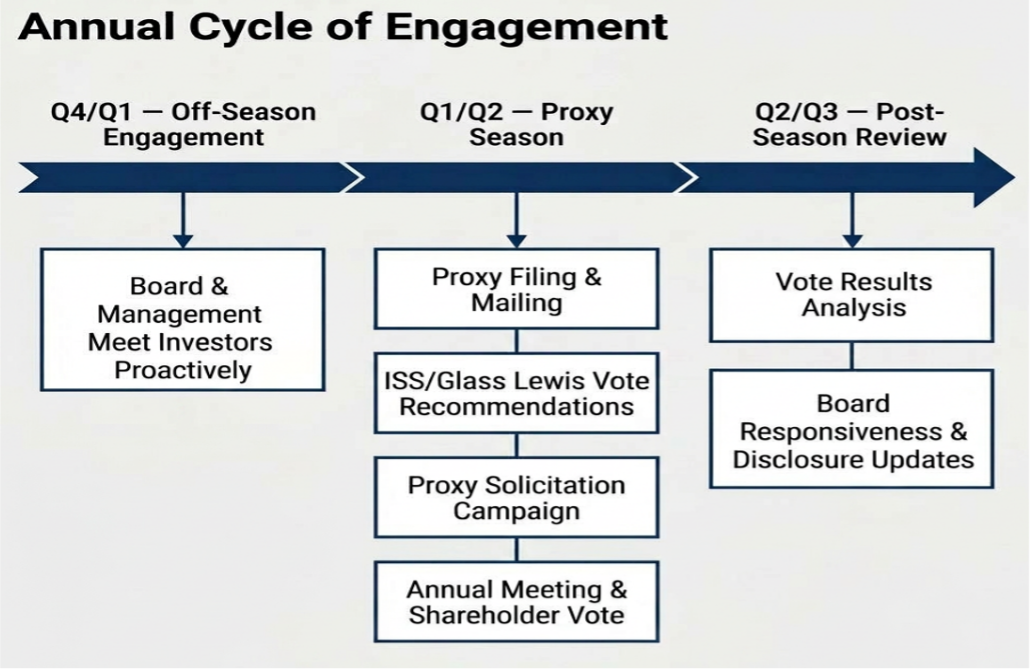

Building on that engagement, BSE is embedded into the company’s annual governance rhythm. Engagement is iterative and responsive, allowing Boards to refine disclosure, strengthen governance practices and address emerging risks well before proxy season.

A typical cadence for companies with a December 31 year‑end includes strategic engagement in the fall, after investors have completed their post‑proxy‑season reviews. These discussions inform Board priorities and disclosures ahead of the following year’s proxy cycle. One structured Board‑Shareholder touchpoint per year is sufficient; during times of change or controversy, more frequent engagement may be warranted.

When done well, engagement strengthens credibility, informs Board decision‑making, and creates a foundation for constructive dialogue long before difficult issues arise.

Unsurprisingly, areas of focus for engagement in recent years have been: Board composition and diversity; climate and environmental oversight; executive compensation; capital allocation; and cybersecurity and AI governance. Topics evolve but always reflect the goals of the stewardship groups, which are to build long-term value creation for stakeholders.

|

BSE – Topics of discussion

|

|

Governance

|

Compensation

|

Strategy

|

- Board composition

- Dual-class share structure

- Proxy access

- Shareholder rights

|

|

|

|

ESG/Sustainability

|

|

Activism Scenarios

|

- Climate targets

- Human capital

- DEI targets

- Supply chain

|

|

- Strategic alternatives

- Spin-offs

- Management changes

- Shareholder proposals

- Board seat demands

|

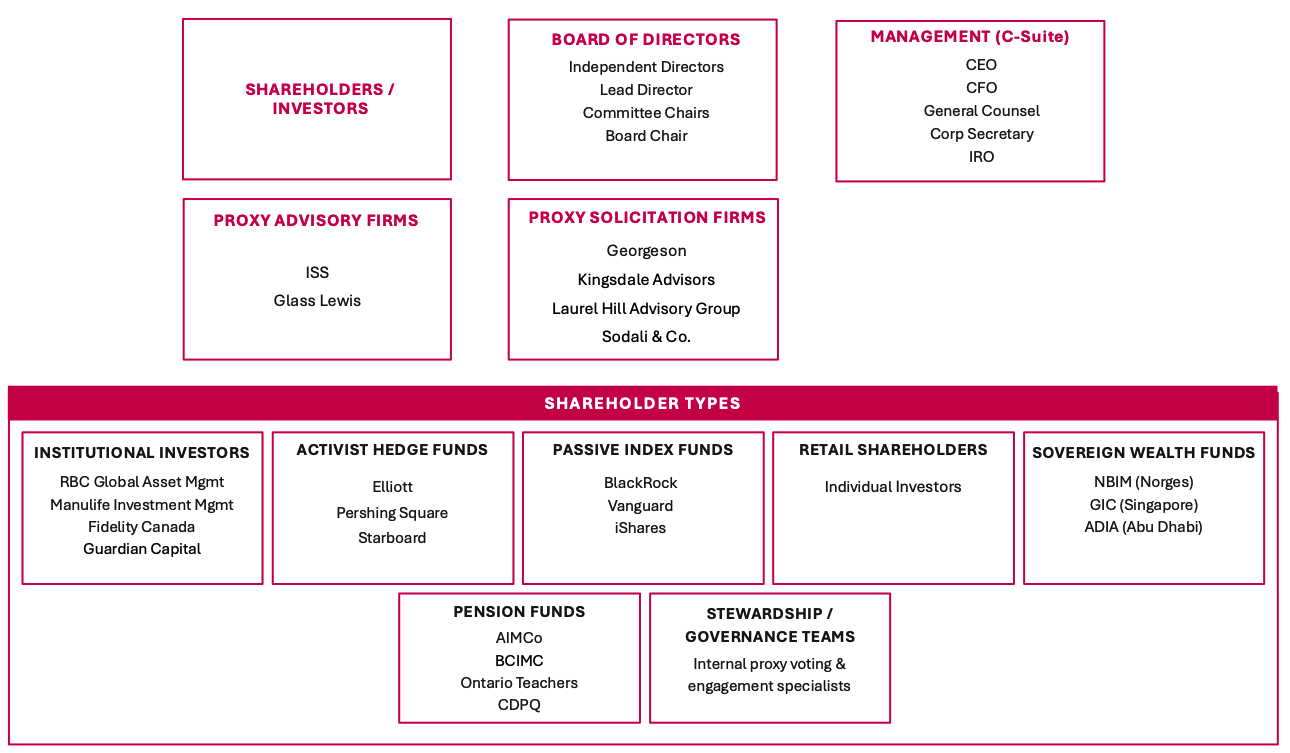

Canadian issuers and their IROs are indeed global, but to understand the unique perspective of their home market, the Canadian Coalition for Good Governance (CCGG) is a great place to start. CCGG was formed almost 25 years ago and represents the interests of large Canadian institutional investors. With Investment Management Corporation of Ontario (IMCO) and Alberta Investment Management Corporation (AIMCo), among CCGG’s over 50 members, more than $6 trillion in assets is represented. The CCGG publishes many excellent resources that are available to the public, and works to engage and influence Canadian issuers to continually improve governance practices broadly, as well as provide recommendations and feedback to specific issuers on certain topics.

BSE is ultimately a Board responsibility and is generally managed through the corporate secretary. However, investor relations plays a critical enabling role. IROs bring deep knowledge of the shareholder base, investor expectations, historical voting outcomes and disclosure practices, making them invaluable partners in preparing Boards for effective engagement.

As Salmon puts it: “IR is the connective tissue – they manage the relationships that Boards and executives don’t have the capacity to maintain. That’s where IR adds real value.”

Great investor relations can go unnoticed. The same is true for strong BSE programs. What doesn’t go unnoticed by investors, management or the Board, however, is a company’s valuation. Strong corporate governance is consistently associated with a higher multiple, lower risk and better financial performance.

Having an excellent governance structure and a strong investor relations function doesn’t preclude an issuer from raising the ire of shareholder activists. Persistent share price underperformance always brings issuers, their management teams and Boards into focus. IROs have a critical role to play here, too, by monitoring trading activity, shareholder movements and the content and tone of investor conversations. IROs who are deeply connected to the capital markets can literally be the canary in a coal mine.

When proxy fights come into the public eye, they can lay bare some of the shortcomings in an issuer’s corporate governance practices. As highlighted in CCGG’s publication, CCGG Investor Perspective 2024 Lookback. Gildan Activewear: A Corporate Governance Case Study, recent Canadian proxy contests underscored the importance of early and ongoing engagement. The Gildan proxy contest illustrated investor expectations around Board continuity, transparency and the ‘no surprises’ principle for long‑term capital providers.

Access to independent directors and proactive engagement were key lessons for issuers. CCGG also notes the importance of stakeholder engagement and corporate culture at Gildan, and the Board’s lack of understanding of the thoughts and needs of its broader stakeholder base. The publication notes, in particular, “One of the lesser reported outcomes of the CEO transition was a reported letter to shareholders from some of Gildan’s executives, urging the reinstatement of the former CEO. This is a somewhat overlooked but important development in the dispute because, if true, it could point to a lack of understanding by the Board as to how the corporation’s culture would be impacted by the replacement of its founder CEO and the abrupt manner in which it took place.”

While IROs are deeply familiar with the capital markets ecosystem, the governance ecosystem operates somewhat differently. At the centre are Boards and shareholders, supported by a network that includes proxy advisory firms and proxy solicitation advisors.

Proxy advisors provide research and voting recommendations that inform many institutional investors’ decisions, while proxy solicitation firms advise issuers on shareholder composition, voting behaviour, governance trends and engagement strategy.

ISS and Glass Lewis, the two largest proxy advisory firms, act to support investors in assessing proxy circulars, including adherence to their respective guidelines, by publishing their recommendations to their client base. Ensuring that your disclosure is sensitive to the requirements of these proxy advisors is key. They will only utilize information that is in the public domain to make an assessment, and the vast majority of asset managers will either vote directly in line with their recommendations or use it as a significant input. Only the largest asset managers have the resources to assess proxies within their own teams.

Ultimately, these guidelines are meant to reflect their clients’ – asset managers’ – evolving views on governance.

Source: Canadian Coalition for Good Governance (CCGG), Annual Report on 2025 Engagement Season, January, 2026, and Building High-Performance Boards, 2024.

The foundation of strong BSE is transparency, preparation and follow‑through. ESG or sustainability reporting allows companies to describe their governance structure, stakeholder engagement and material risks and opportunities in detail.

RioCan Real Estate Investment Trust’s Board of Trustees continues to expand its BSE over the last few years. As Jennifer Suess, Senior Vice President, General Counsel, ESG and Corporate Secretary at RioCan, notes, “We have found the consistent ongoing dialogue embedded in the BSE process allows for meaningful conversations, and it builds trust over time.” When trust has been built, it allows for conversations that can sometimes be tricky to start from a place of goodwill, rather than enmity.

IROs are well able to lead the development of issuers’ disclosure and communication material. It can be difficult to find examples of Board-Shareholder engagement materials online; however, TC Energy published a presentation, Sustainability Highlights for Investors, in February of this year.

Consistent with the goal of long-term value creation for companies, the success of BSE is not defined by winning a single vote but by building durable trust that supports long‑term value creation and reduces friction during periods of stress. That sounds a lot like IR.

As Salmon noted, “When engagement becomes ongoing and two‑way, investors are far more open to those conversations – even on sensitive or contentious issues. The goal is continuity: reinforcing your story over time and showing how governance decisions connect to strategy, risk and values.”

For issuers that haven’t embarked on BSE, getting started is fairly straightforward. Shareholder base analysis, creating an engagement calendar and cadence, preparing the content and continuously monitoring the broader environment are all important aspects of a BSE exercise, and importantly, IROs can support or lead these efforts.

IROs would be well served by actively engaging in BSE. It will increase visibility with key stakeholders, and provide meaningful benefits to executive leaders, the Board and shareholders.

Six Steps of BSE

More About IR focus