Plummeting oil prices may create a quandary for extractive companies when it comes to executive compensation. Should CEOs and others whose pay is tied to performance suffer because their companies’ profits fell when oil prices dropped? Or should Compensation Committees use ‘discretion’ and bolster executives’ bonuses and then let IROs and others deal with any shareholder fallout?

Whichever route a company chooses, IROs may find themselves in the hot seat when it comes to explaining these choices to investors. “Using discretion is still important in compensation plans because formula results might not always be right,” says Andrew Stancel, Consultant at Toronto-based Meridian Compensation Partners. And yet he acknowledges that “discretion is very controversial when it’s used to override the plan formula and increase payouts as opposed to decrease payouts.”

For IROs, the true challenge will lie in understanding the guidelines regarding how discretion is used and explaining decisions to investors clearly and forthrightly. “The important thing is to have some guidelines around how discretion is used,” says Stancel.

Although conversations about discretionary payouts are particularly thorny, IROs could also improve the way they explain executive compensation policies in general to investors.

Nearly half of institutional investors believe that corporate disclosure with respect to executive compensation should be clearer and easier to understand, according to research released in February by the Stanford Graduate School of Business. Shareholders in the Stanford study were particularly dissatisfied with CEO compensation disclosure.

For IROs reviewing compensation flashpoints in order to converse with shareholders more knowledgeably, maintaining an open mind is paramount. “Remember that you don’t always know what you don’t know,” says Ian Robertson, Vice President, Communications, at Kingsdale Shareholder Services. “We always run into managements that tell us shareholders love them, but when we talk to shareholders, that’s not always the case.”

Robertson points out that many shareholders are reticent about voicing pay concerns simply because talking about salaries is socially taboo. “It’s hard for a shareholder who is friends with the CEO to say: ‘Look, I think your pay package is ridiculous, especially vis-à-vis your company’s performance, and as a shareholder, I think I’m getting ripped off.’” He adds: “So even if you don’t think you have a problem, you should always be ready for the questions.”

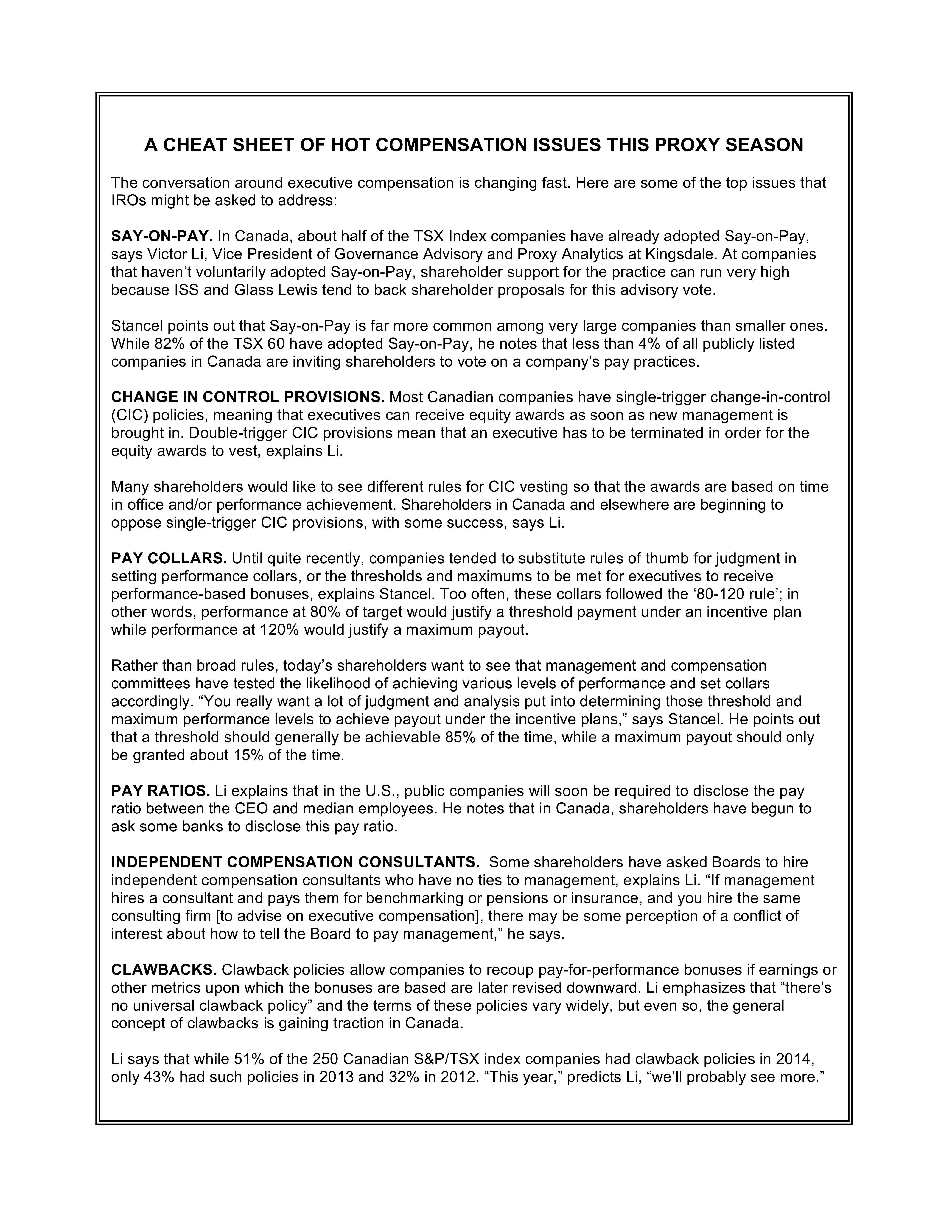

What Shareholders Want

Rudy Sankovic, Senior Vice President, Investor Relations, at TD Bank Group, says that in Say-on-Pay votes his company’s executive compensation plans have garnered shareholder support in the 95% acceptance range; levels he believes come from the company’s efforts to provide plain-language disclosure. He also notes that TD invites shareholders to discuss compensation directly with the Board without IR or management present. “We take a lot of time in outlining pay and sitting down with shareholders,” says Sankovic. “As a result, we don’t get the same kind of pushback [that some other companies do].”

Sankovic suggests that strong performance also helps insulate IR and executives from compensation complaints. He points out that TD boasts 12% growth compounded annually for the past 15 years. “Management is being rewarded for outperformance, and when you have that, you have fewer issues with things like compensation.”

“When most investors talk to us about compensation, they ask: ‘What drives compensation? And what are the metrics you use to measure compensation?’” says Sankovic. “They’re less worried about the dollars paid and more about the metrics driving compensation.”

Stancel has observed the same: “Investors want to understand the goal-setting process at a company.” He continues: “If investor relations officers can understand how companies set their compensation goals and targets, that’s really important.” Gone are the days of all companies assigning performance ranges mechanically. Today, investors want to delve into the ‘whys’ and ‘hows’ of compensation decisions.

When responding to investor questions, Robertson urges IROs to listen carefully and engage in a true dialogue. “Spend time listening to exactly where investors are coming from and understand not only their concerns but their expectations,” he says. “Explain the decision-making process to get the compensation you did and always tie it back to the company’s overall strategic goals and make sure there’s a clear alignment.”

Robertson points out that after Barrick Gold received 14.8% support on its 2013 Say-on-Pay, the company cut its CEO’s pay and embarked on an investor roadshow to hear shareholder concerns and better explain compensation practices. As a result, in 2014 Barrick Gold saw support for its compensation packages rise above 80%.

Ken Hugessen, Partner and Founder of Hugessen Consulting in Toronto, urges IROs to delve into the intricacies of their companies’ pay practices so that they can answer inquiries intelligently. “It’s important that IROs be intimately involved in the disclosure of executive pay. It’s very hard to explain something that’s been disclosed if you don’t have an intimate knowledge of all aspects,” he says.

Finally, Andrea Boctor, Head of the National Pensions and Benefits Practice Group and Partner at Stikeman Elliott LLP, believes that IROs discussing compensation with investors, should focus on “process,” rather than dollars-and-cents results. “In my experience, compensation decisions are not made lightly,” says Boctor. “If appropriate, I’d message that the process is rigorous and the result is reasonable and justifiable based on that process.”

Looking Ahead: Rethinking the Compensation Message

Responding to retail investors harbouring compensation concerns can require a slightly different approach. “Retail investors,” says Hugessen, “are more fussed about the level of executive pay. They’re asking less why your company paid this amount and more: Why do we pay CEOs as much as we do?”

Kingsdale’s Robertson agrees, adding: “Your retail investor was bruised by the financial crisis and is skeptical of corporate leaders, thanks to Enron.” He continues: “Long, detailed answers tend to signal to [retail investors] that you’re trying to hide something.”

In the final analysis, says Stancel, “the proxy circular should really be a public relations piece, used to tell and sell the pay story.” He is convinced that too many proxies are wordy and difficult to understand. And in fact, the Stanford study found that 55% of investors believe that the typical proxy is too long.

What investors really want, agree the experts, is a simple, sincere explanation of a company’s compensation philosophy that uses clean graphics and responds to their concerns in plain English.